While studies continually show that a college degree has substantial financial benefits to most graduates, more and more millennials find themselves asking – Is a college degree worth it?. This is often after many years of struggling to pay back their student loans.

In the US, college costs have more than doubled in the last decade, sending Americans – mostly millennials – past the $1.5 trillion mark in aggregate federal student loan debt.

At the current growth rate, the collective student loan debt could reach $2 trillion by 2024, according to SavingforCollege.com. The average amount of student loan debt per borrower stands at $37,584.

What makes the situation frightful is that many people take out student loans with an overestimated view of their future earnings.

According to a survey by SoFi, about 50% of the respondents said that the biggest mistake they made with their student loan was overestimating the salary of their first job.

In This Article

Consequences of student debt

While the advantages of having a college degree are indisputable, taking on a lot in student debt will put a massive burden on you for the rest of your life.

It will cause you to put off significant life events to concentrate on paying down your student loans. For instance, student loan debt lowers your credit score affecting your ability to borrow money.

Additionally, you will not be able to qualify for a mortgage until your debt-to-income ratio is below 43%.

According to ACA International, 18% of people paying off student debt have to live paycheck to paycheck because they spend most of their salary on loan repayment.

How to minimize your student loan debt.

1. Don’t overborrow

It’s tempting to borrow more than necessary to make life in college comfortable. However, this decision could have adverse effects on the quality of life after college.

If your first job is only an entry-level one, you may struggle to make your monthly loan payments.

Additionally, the more you borrow, the longer you’ll be in debt, thus postponing major life milestones such as buying a house.

2. Choose a cheaper college.

Given a chance to choose between two colleges of comparable education quality, choose the cheaper one – unless the expensive one offers study programs with better career prospects.

With more than 4000 universities to choose from, you’re sure to find one that fits your budget.

3. Transfer to University after two years of community college.

Universities are costly.

Consider taking your first two years at a community college and then transferring to the University of your choice.

Community colleges are way cheaper and will save you a lot in tuition fees, not to mention how much you could save on living expenses if you choose to attend a local one.

Before embarking on this plan, check whether the universities you are interested in accept credit transfers from community colleges.

4. Apply for scholarships

Study financial aid and scholarships will help significantly minimize your student loan debt.

While filling in applications and writing essays for scholarships can be time-consuming, it will substantially reduce the amount of money you’ll need to borrow if you do get a scholarship.

5. Attend an online college

The average cost of a degree from a brick-and-mortar college is $85,000. Compare the hefty price to an online college degree which costs roughly $30,000, and you’ll want to reconsider going off to college.

The freedom to learn whatever you want from the comfort of your home and at less than half the cost of an ordinary college makes attending an online college ever so lucrative.

Online Colleges are increasingly becoming popular, with more and more colleges making their programs accessible online.

Even if you decide to attend a brick-and-mortar college, you could still save a lot on living expenses if you choose to take the online programs and live at home.

6. Work while you attend college.

When it comes to combining work and studies, you have several options:

- Part-time work and part-time study.

- Full-time work and part-time study.

- Part-time work and full-time study.

The third option may seem too ambitious, but it’s not unattainable. You can easily pull it off by combining it with a strategy I explained earlier: online college.

In addition to paying less in tuition fees, attending an online college will allow you the flexibility and freedom to take up a part-time job.

Here are the perks of this strategy: you’ll be able to earn an income, save on living expenses by choosing to live at home, and save on tuition fees by attending an online college.

Doesn’t that sound like a good deal?

Hey, you might even end up not needing a study loan. Imagine the possibility of graduating debt-free.

It is worth noting that this strategy requires making sacrifices – like deciding to continue living with your parents – and, most importantly, a high level of discipline.

7. Military service

The military provides education benefits to its service members in the form of financial aid, college funds, and loan repayment programs.

According to Today’s Military:

“Tuition Assistance pays for up to 100 percent of the cost of tuition or expenses, up to a maximum of $250 per credit and a personal maximum of $4,500 per fiscal year per student. This program is the same for full-time members in all Military Services.”

While there are conditional requirements to qualifying for these benefits – such as a minimum amount of time served – joining the military service can be a great way to finance your entire college education.

Before taking a student loan

So, you didn’t find a way to finance 100% of your studies and still had to take out a loan, that’s ok. Even with the above strategies, you might still need to take a loan to finance part of your studies. The most important thing is to avoid getting yourself neck deep into debt. Here are factors to consider before signing those loan documents.

1. Discuss it with your parents or a professional

According to a student lending survey conducted by Citizens Bank, 53% of the respondents believe that they would have incurred less debt if they discussed all possible financing options with their parents before taking on student loan debt.

If talking to your parents is not an option, you can find a finance-savvy relative, a student advisor/counselor, or a financial advisor.

2. Understand the true cost of a student loan and your repayment options.

In addition to principal payments, student loans come with additional costs such as loan fees and interest. Be sure to compare as many loan offers as possible to find the loan with the most favorable terms, low fees, and the least monthly payments.

When it comes to repayment plans, there are several ways to pay back your loan. Here are some of the options:

- Standard repayment: Make equal payments for a maximum of 10 years.

- Graduated loan repayment plan: Start with small repayments, which gradually become larger with time.

- Extended loan repayment plan: Pay back within 10 to 30 years.

- Income-driven repayment plan: Depends on how much you earn. Payments are set between 10% and 20% of your income.

3. Budget

Create a budget before borrowing. Generally, student loan limits are set way above what students need.

A budget will help you determine exactly how much you’ll need to cover both your tuition fees and living expenses. Consequently, it will ensure that you don’t over-borrow and therefore minimize your student loan debt.

4. Choose a career in high demand.

Last but not least, before you get into college, make sure that the time and money you’re about to spend will be worth your while.

Choose a career path that will lead to a high-paying job that’s in high demand.

Failure to do so will result in lots of regrets. So you have to be sure.

Examples of jobs that will be in demand in the next five years are:

- Registered Nurses

- Software Developers

- Civil Engineers

- Accountants and Auditors

- Physicians and Surgeons

- Dental Hygienists

- Financial Analysts

- Dentists

- Information Security Analysts

- Post Secondary Education Teachers

Conclusion on how to minimize your student loan debt.

Unlike popular belief, a student loan is not the only way to finance your studies.

If you consider the consequences of graduating with a huge student loan debt, it is unquestionably worth looking into different options to fund your education.

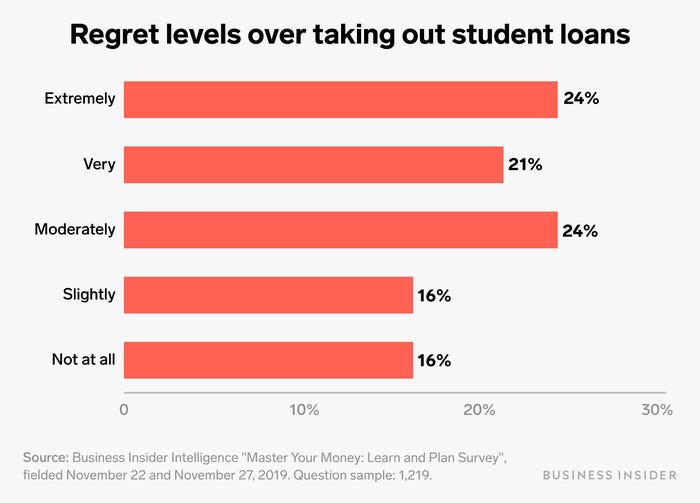

According to the survey by Citizens Bank, a startling 74% of Americans with student loan debt wish they could have done a lot more to minimize the burden of their student loans.

I’ve mentioned seven ways on how to minimize your student loan debt. In addition to these, I’ve also included four things to consider before taking a loan. Carefully consider all of them and select the most reasonable alternatives for you.